The Sudden Notice: What’s Really Driving Resin Price Hikes?

"We are raising prices again." Why do these notices always seem to arrive out of the blue?

You open your inbox and a specific subject line catches your eye: “Notification of Price Revision for Resin Materials (Request).” Your first thought is likely, “Here we go again.” You click the email, and there it is - the standard boilerplate text about soaring raw material costs and a request for a double-digit percentage hike starting next month. Yet, the attached document only lists the new unit prices by grade. It fails to mention the most critical details: When exactly did costs spike? Why was this specific percentage chosen?

In the world of procurement, these "sudden price increase notifications" are all too common. In this column, we will trace the chain reaction from upstream to downstream—following the flow of costs from their source to your desk—to understand how and why these price hikes occur.

■Japan and Middle-East

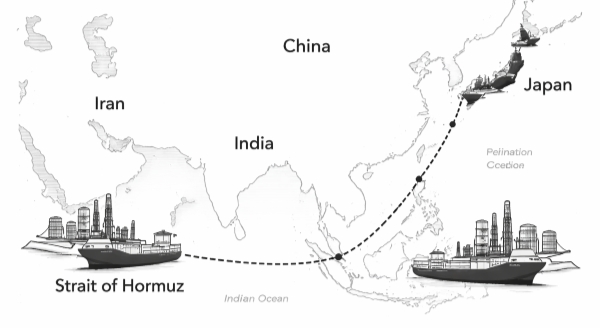

The Strait of Hormuz: A Critical Bottleneck for 70% of Naphtha Imports

The current procurement risks for resin materials stem largely from heightening tensions in the Middle East, which are casting a long shadow over Japanese manufacturing. The numbers make the gravity of the situation clear.

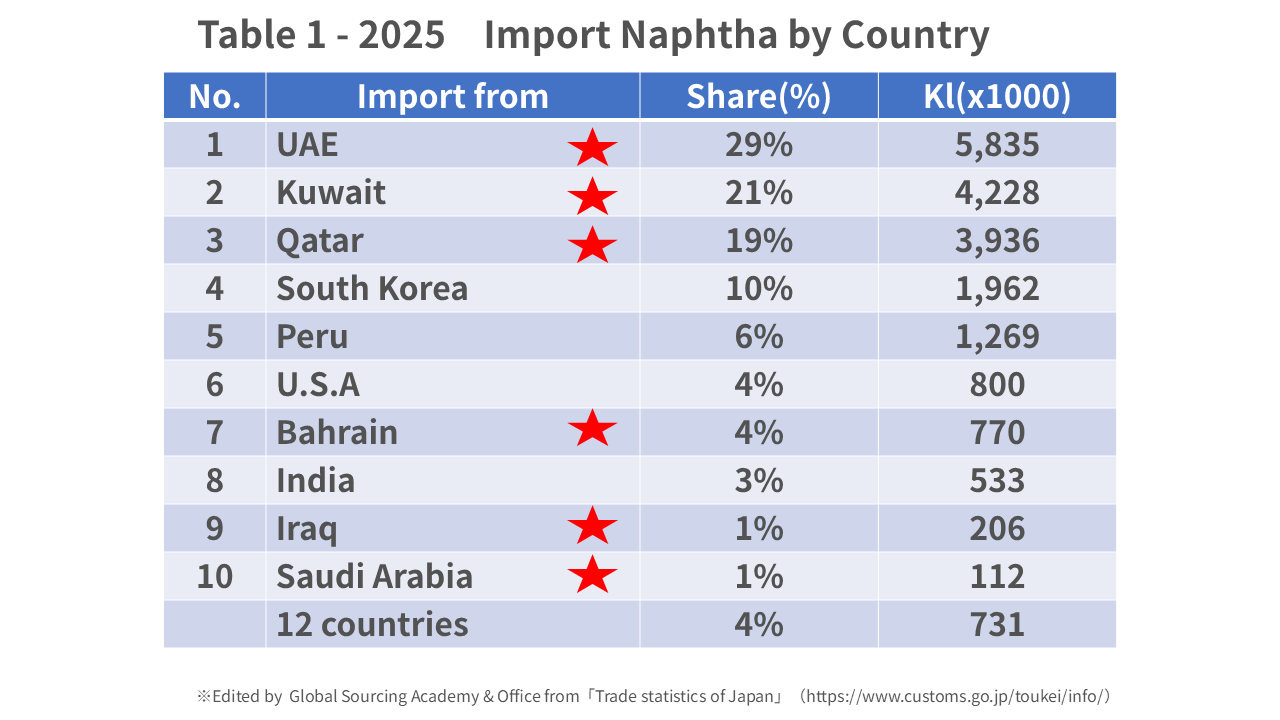

According to 2025 trade statistics from the Ministry of Finance (based on HS Code 2710.12.181), Japan's naphtha supply is heavily concentrated in three countries.

the UAE (29%), Kuwait (21%), and Qatar (19%). Together, these account for roughly 69% of imports. When you include Iraq, Bahrain, and Saudi Arabia, Japan’s dependency on the Middle East exceeds 75% (See Table 1).

Every tanker originating from these nations must pass through the Strait of Hormuz, located at the mouth of the Persian Gulf.

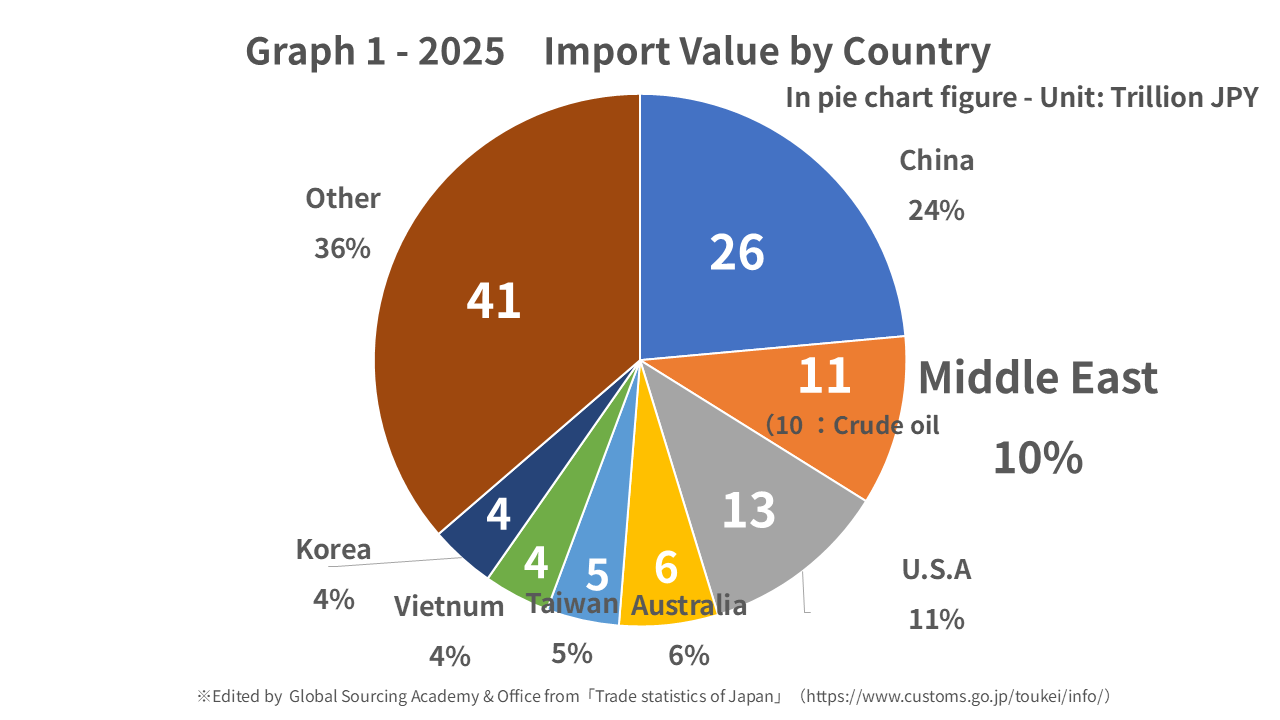

While this 50km-wide strait may not be the global bottleneck for all petroleum products—since Europe’s dependency on the region is lower—for Japan, it is a literal lifeline. Middle Eastern imports account for approximately 10% of Japan’s total import value, dominated by oil and crude-related products worth roughly 10 trillion yen (See Graph 1). This region provides about 94% of Japan's crude oil. Considering that domestic naphtha (which accounts for about 30% of total supply) is refined from imported crude, the Middle East is quite literally the jugular of Japan's energy and material supply.

■Market & Weak Japan Yen

Volatility as the New Normal: The 2022 Surge and Future Risks

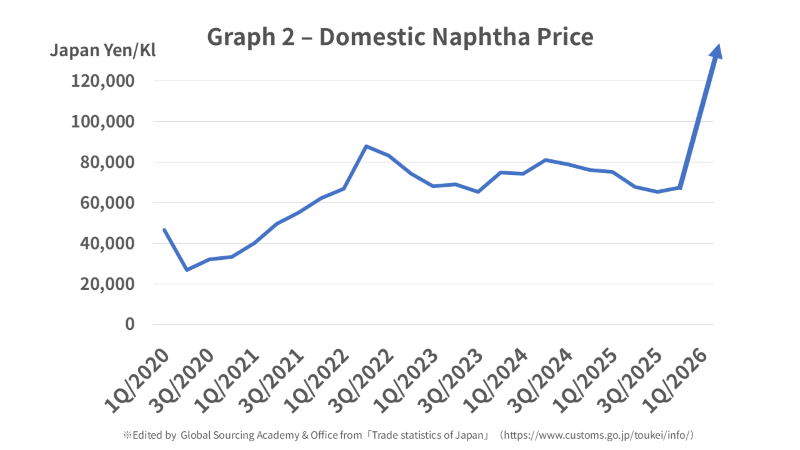

We conceptually understand that "if crude oil goes up, naphtha follows." However, seeing the actual magnitude of these fluctuations is enough to make any professional pause.

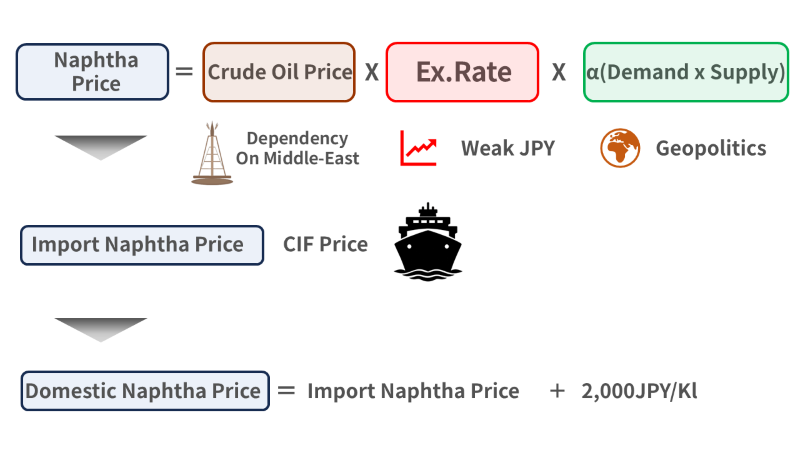

Looking back at naphtha prices between 2020 and 2025, the volatility is staggering. In Q2 2020, prices plummeted to approximately 27,000 yen/kl due to the collapse in demand during the pandemic. Just two years later, in Q2 2022, they skyrocketed to roughly 88,000 yen/kl—more than a threefold increase. This was a "double punch" delivered by the global market chaos following Russia's invasion of Ukraine and the rapid depreciation of the yen. While prices stabilized somewhat in 2025, hovering around 65,000 to 68,000 yen/kl, they are far from "stable." Current levels remain more than 40% higher than pre-pandemic levels (approx. 46,000 yen/kl in 2020).

The price trends in Graph 2 are simplified by adding 2,000 yen/kl to the quarterly average import naphtha price.

For procurement teams, the key takeaway is not just the absolute price, but the speed and scale of the swings. A move that triples the price in just eight quarters can vaporize a mid-term profit plan overnight. Because naphtha is traded in dollars, even if crude prices remain flat, a weakening yen automatically drives up import costs (See Image 1).

The 2022 spike represented a worst-case scenario: a simultaneous rise in crude prices and yen depreciation. Today, we are seeing those same conditions align once again.

■Toward plastic resins

From Crude to Resin: Dissecting the "Transmission Lag"

We have established the mechanism by which Middle Eastern risk moves naphtha prices. The next logical question is: "When and how does that volatility reach specific resin materials?" The answer reveals a critical nuance for procurement strategy.

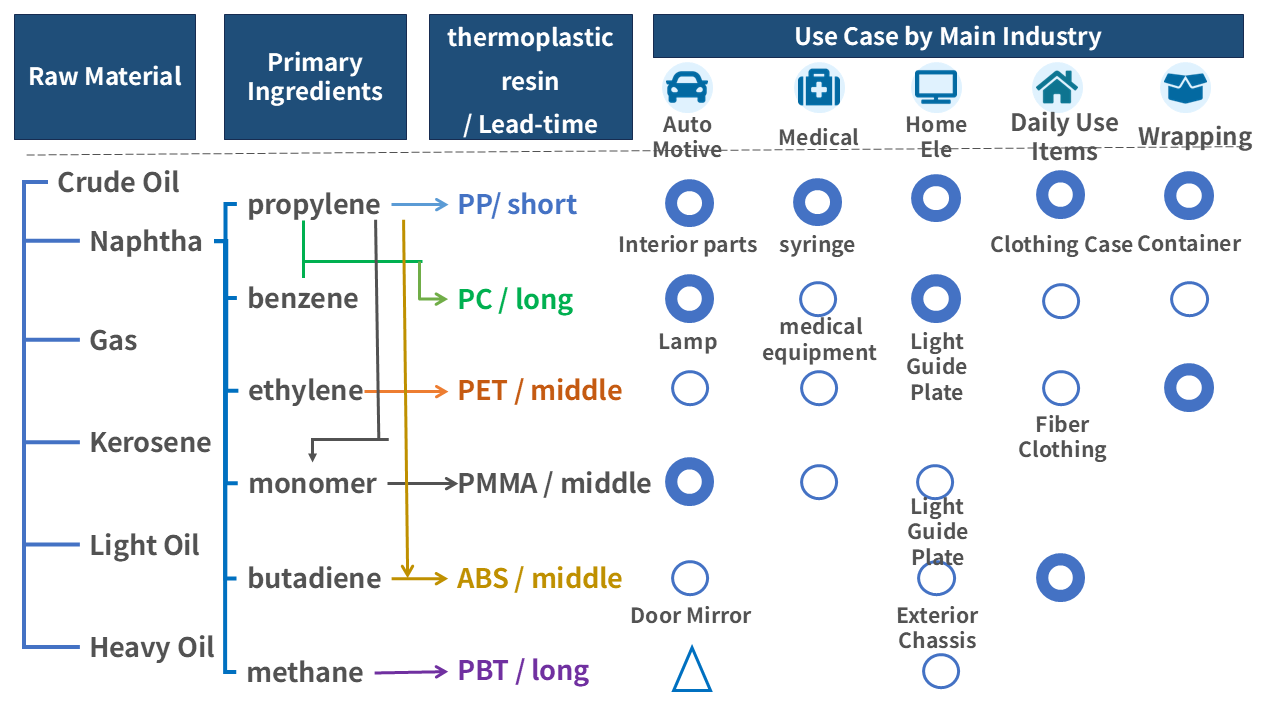

Let’s simplify the journey from crude oil to plastic parts. Refining crude yields naphtha. Cracking or reacting naphtha produces monomers such as ethylene, propylene, benzene, and butadiene. These are then polymerized and processed into the resin materials we procure.

However, even though they share the same "parent" (naphtha), the timing of price reflection varies by resin. For instance, Polypropylene (PP) is produced through a relatively simple process (Crude → Naphtha → Propylene), resulting in a short manufacturing lead time and faster price reflection. Conversely, materials like PBT or PC often experience a significant time lag due to complex downstream processing and intermediate inventory stages.

While new pricing is typically negotiated for the upcoming quarter or half-year, some "sudden" notices may include opportunistic hikes based on immediate market sentiment. If we, as procurement professionals, fail to verify these claims against theoretical values and clarify which period the notification actually applies to, we risk falling into reactive, short-sighted negotiations.

■Middle-East Now !

Mapping Your Middle East Supply Chain Dependencies

In this column, we have analyzed the "cost perspective" by following the numbers from upstream to downstream. However, looking at the current reality in the Middle East, the Strait of Hormuz is effectively facing a logistical shutdown.

While ports in Oman and Yemen are being considered as alternatives, industry insiders warn that their limited scale makes them inadequate as long-term solutions. Furthermore, shipping companies are expected to announce Emergency Fuel/Bunker Surcharges. Given that the Middle East serves as a global supply hub between Europe and Asia, the impact on the entire supply chain is profound.

While daily operations are demanding, it is imperative to prioritize a "supply chain audit" of critical components (especially non-multi-sourced items) that pass through the Middle East, in collaboration with Tier 1 suppliers. A crude oil tanker from the Persian Gulf arrived in Japan on Sunday, March 22nd. The question we must all ask is: when will the next one be able to dock?

Procurement and management consulting, advisory services